Micron has officially announced the end-of-life (EOL) phase for DDR4 memory, marking the full transition of all three major DRAM manufacturers (Samsung, SK Hynix, Micron) to DDR5 and more advanced process nodes. This decision will exacerbate supply-demand imbalances, trigger significant price volatility, and profoundly impact the entire industry chain.

● EOL Timeline: Micron has sent DDR4/LPDDR4 discontinuation notices to PC, smartphone, and data center clients. Consumer – grade product production will be cut in the next three quarters, with shipments ceasing in 6 – 9 months. The automotive, industrial, and networking sectors will have limited supply. Samsung stopped new DDR4 orders in late 2024, plans a full stop in 2025; SK Hynix reduced DDR4 capacity to 20%; CXMT expects to exit DDR4 by 2026.

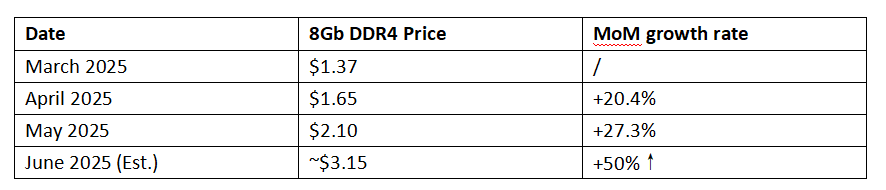

● Market Impact: From January to June 2025, DDR4 spot prices rose 89% cumulatively. 8Gb DDR4 prices increased from $1.37 in March to $2.10 in May, with a possible 50% hike in June. The shortage is driven by capacity cuts, stockpiling due to the U.S. – China tariff grace period, and inelastic demand from industrial/automotive sectors slow to migrate to DDR5.

● Supply Chain Shifts: Micron is restructuring to focus on DDR5, LPDDR5, and HBM for AI PCs and data centers. This shift prompts other manufacturers like Taiwan’s Winbond and Nanya to expand DDR4 production, and Chinese manufacturers like CXMT are also looking to fill the supply gap.

● Technology Transition & Industry Effects

DDR5 Acceleration:

Advantages: 6400 MT/s bandwidth (2× DDR4), 20% lower power; ideal for AI/data centers.

Penetration: To exceed 50% market share in 2025; Intel/AMD platforms now DDR5-exclusive.

Short-Term Challenges:

Rising Repair/Upgrade Costs: Legacy systems face expensive DDR4 replacements.

Price Pass-Through: PC/server brands (e.g., Apple’s MacBook) eliminating 8GB configurations amid cost pressures.

● Outlook

-Near Term (1–2 Years): DDR4 shortages persist; prices remain elevated, driven by tariffs (if July 2025 implemented) and industrial demand.

-Long Term (3–5 Years): DDR4 phased out; DDR5 dominates mainstream; HBM demand explodes for AI, fueling capacity wars among manufacturers.

DDR4 Price Trends (2025)

● Conclusion

Micron’s DDR4 exit marks a critical inflection point in memory technology. Short-term price turbulence and supply chain realignment will give way to long-term industry upgrades toward high-performance DDR5/HBM. Traditional sectors (industrial/automotive) must accelerate adoption, while Chinese memory makers gain expansion opportunities. Over the next six months, DDR4 scarcity premiums and DDR5 cost-performance sweet spots will coexist, requiring strategic balancing across the value chain.