- Samsung Activates Emergency Plan, Signs $7.27 Billion Credit Agreement

-Samsung signed a credit agreement with South Korean Commercial Banks to optimize funding costs and address market challenges.

-This move reflects Samsung’s cautious stance amid intensifying competition in the memory market.

2. Old Rival SK Hynix Leads in the HBM Market

SK Hynix Surpasses Samsung with HBM Technology:

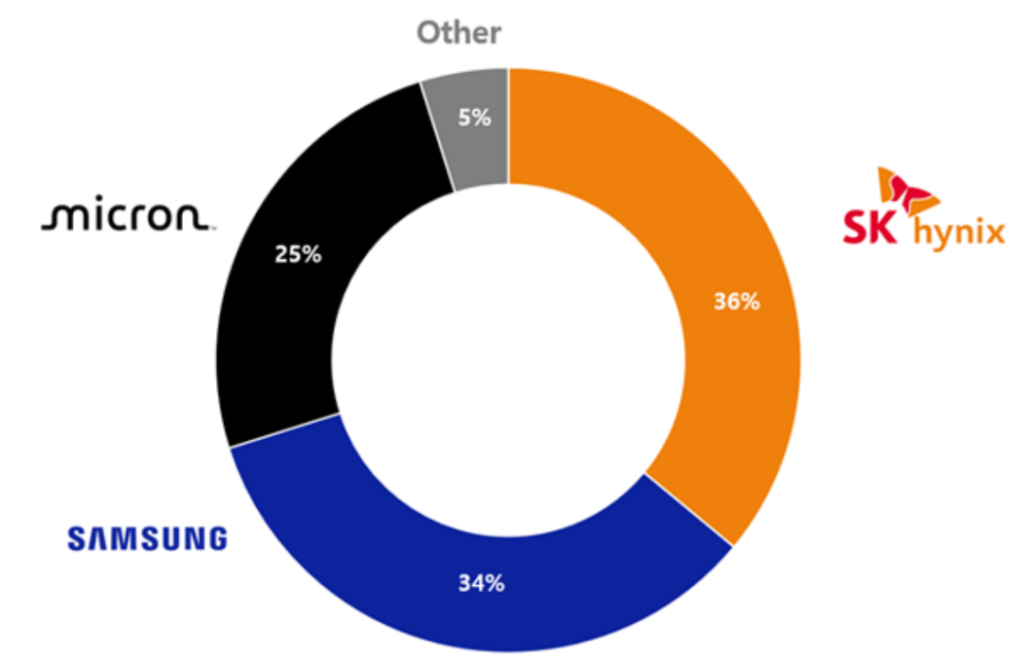

– In Q1 2025, SK Hynix became the global DRAM revenue leader with a 36% market share, leaving Samsung behind.

– Demand for HBM (High Bandwidth Memory) has surged due to AI, with SK Hynix holding over 50% of the market.

Samsung Lags Behind in HBM3E Competition:

– Failed to pass NVIDIA’s HBM3E quality tests, trailing behind SK Hynix and Micron.

– Shifted personnel from its semiconductor foundry division to HBM development, betting on HBM4 technology and planning to integrate its own logic chips for performance gains.

3. New Competitors: Rapid Rise of Chinese Memory Manufacturers

– Narrowing Technology Gap: Chinese manufacturers are only 3-4 years behind Samsung in HBM technology.

– DRAM Capacity Expansion:

– Chinese manufacturers plan to increase DDR5/LPDDR5 production to 110,000 wafers/month (6% of global capacity) by the end of 2025.

– One Chinese memory company expects a 68% growth in DRAM output in 2025, potentially catching up with Micron.

Leadership in Advanced Packaging Technology:

– Chinese companies lead in hybrid bonding patents (119 vs. Samsung’s 83).

– This technology enhances HBM stacking layers and yield, potentially reshaping market competition.

4. Samsung’s Countermeasures

– DRAM Production Adjustments:

– Began mass production of 1c DRAM, aiming to boost capacity to 40,000 wafers/month in H2 2025.

– Phasing out some DDR4/LPDDR4 products to focus on more advanced processes.

– Seeking External Collaboration: Partnering with TSMC to develop HBM4 base chips, breaking from its traditional closed approach.

– NAND Market Adjustments:

– Samsung remains the NAND market leader, but revenue fell 25% due to weak demand.

– Plans to discontinue MLC NAND production and raise prices, pushing customers to seek alternatives.

( 1Q25 Nand flash Revenue for the top 5 companies)

5. Future Challenges and Outlook

– The HBM market is growing rapidly, but Samsung must make breakthroughs in HBM4 to avoid falling further behind.

– Chinese memory manufacturers’ advancements in capacity and technology could squeeze Samsung’s traditional memory chip market.

– Samsung is responding with financial optimization, production adjustments, and open collaboration, but its ability to regain leadership remains uncertain.

Conclusion: Samsung faces dual pressure from SK Hynix and Chinese competitors, particularly lagging in HBM. Through financing, technological transformation, and external partnerships, Samsung is striving to turn the tide. However, intense competition means the market landscape could continue evolving.